Please refer to important disclosures at the end of this report

1

Incorporated in 2008, eMudhra is largest licensed Certifying Authority in

India with a market share of 37.9% in the digital signature certificates market

space in FY2021 having grown from 36.5% in FY2020. It is engaged in the

business of providing Digital Trust Services and Enterprise Solutions to

individuals and organizations functioning in various industries. It has strong

digital signature certificate expertise and is the only Indian company to be

directly recognized by renowned browsers and document processing

software companies such as Microsoft, Mozilla, Apple, and Adobe, allowing

it to sell digital identities to individuals and organizations worldwide and issue

SSL/TLS certificates for website authentication.

Positives: (a) Largest licensed Certifying Authority in India (b) One stop shop

solution provider in secure digital transformation (c) Diverse, longstanding,

and growing customer base (d) Partnerships with leading Indian and global

channel partners and enterprise solution partners. (d) Experienced

promoter, board of directors and senior management team

Investment concerns: (a) Success largely dependent on company’s ability

to anticipate, adapt and respond effectively to the technological changes,

evolving industry standards and changing regulations as well as on success

of its R&D. (b) High Dependence on technology for carrying out its business

activities. (c) Highly competitive industry

Outlook & Valuation: eMudhra has an established position as licensed CA

with a strong network of channel partners, a diverse customer base and it

will be using part of the IPO proceeds to grow in overseas markets as well

improve its data center infrastructure. However, the scale of operation is

relatively modest and digital security and paperless transformation market

is highly competitive. At the upper end of the price band, the post issue FY22

annualized P/E works out to 49.0x which we believe is factoring the positives.

Hence, we recommend a Neutral rating on the issue.

Key Financials

Y/E March (` cr)

FY2019

FY2020

FY2021

9MFY22

Net Sales

102

116

132

137

% chg

--

14.6

13.0

--

Net Profit

17

17

17

31

% chg

--

(4.5)

4.9

--

EBITDA (%)

31.7

27.4

30.3

35.9

EPS (`)

2.2

2.1

2.2

3.9

P/E (x)

114.6

120.1

114.5

--

P/BV (x)

26.4

21.7

18.6

--

ROE (%)

23.1

18.1

16.3

--

ROCE (%)

15.0

11.5

13.1

--

EV/EBITDA

62.8

63.6

51.1

--

EV/Sales

19.9

17.4

15.5

--

Angel Research; Note: Valuation ratios based on post-issue shares and at

`

256per share.

NEUTRAL

Issue Open: May 20, 2022

Issue Close: May 24, 2022

Fresh Issue: `161cr

QIBs 50%

Non-Institutional 15%

Retail 35%

Promoters 61.0%

Public 39.0%

Post Issue Shareholding Pattern

Post Eq. Paid up Capital: `23.05cr

Issue size (amount): `413cr

Price Band: `243-256

Lot Size: 58 shares

Post-issue mkt.cap: `1,905*– 1,999cr**

Promoter holding Pre-Issue: 71.19%

Promoter holding Post-Issue: 61.03%

*Calculated on lower price band

** Calculated on upper price band

Book Building

Offer for sale:`252cr

Issue Details

Face Value: `5

Present Eq. Paid up Capital: `36cr

Yash Gupta

yash.gupta@angelbroking.com

eMudhra Limited IPO

f

IPO Note |IT

May 18, 2022

eMudhra Limited | IPO Note

May 18, 2022

2

Company background

eMudhra is a licensed certifying authority under the Information Technology

Act,2000, founded in 2008 from the seed of digital signatures. eMudhra has

since grown to establish strong roots in solutions providing security to

enterprises and end consumer for online transactions and in paperless

transformation. eMudhra’s products include digital signature certificates,

authentication solutions, paperless office solutions and Certifying Authority

solutions. It also offers solutions around PKI technology and digital

transformation.

eMudhra is the largest licensed Certifying Authority in India with a market

share of 37.9% in the digital signature certificates market space in Financial

Year 2021 having grown from 36.5% in Financial Year 2020.

Its two business verticals are Digital Trust Services and Enterprise Solutions. As

part its Digital Trust Services, it issues a range of certificates including

individual/organizational certificates, SSL/TLS certificates and device

certificates (used in IoT use cases) to build a digital trust backbone. Under

its Enterprise Solutions vertical, company offers a diverse portfolio of Digital

Security and Paperless Transformation Solutions, complementing its Digital

Trust Services business, to customers engaged in different industries, thereby

making the Company a ‘one stop shop’ player in secure digital

transformation.

Issue details

eMudhra is raising ₹239-`252cr through OFS and ₹161cr through Fresh

Issue in the price band of ₹243-₹256per share.

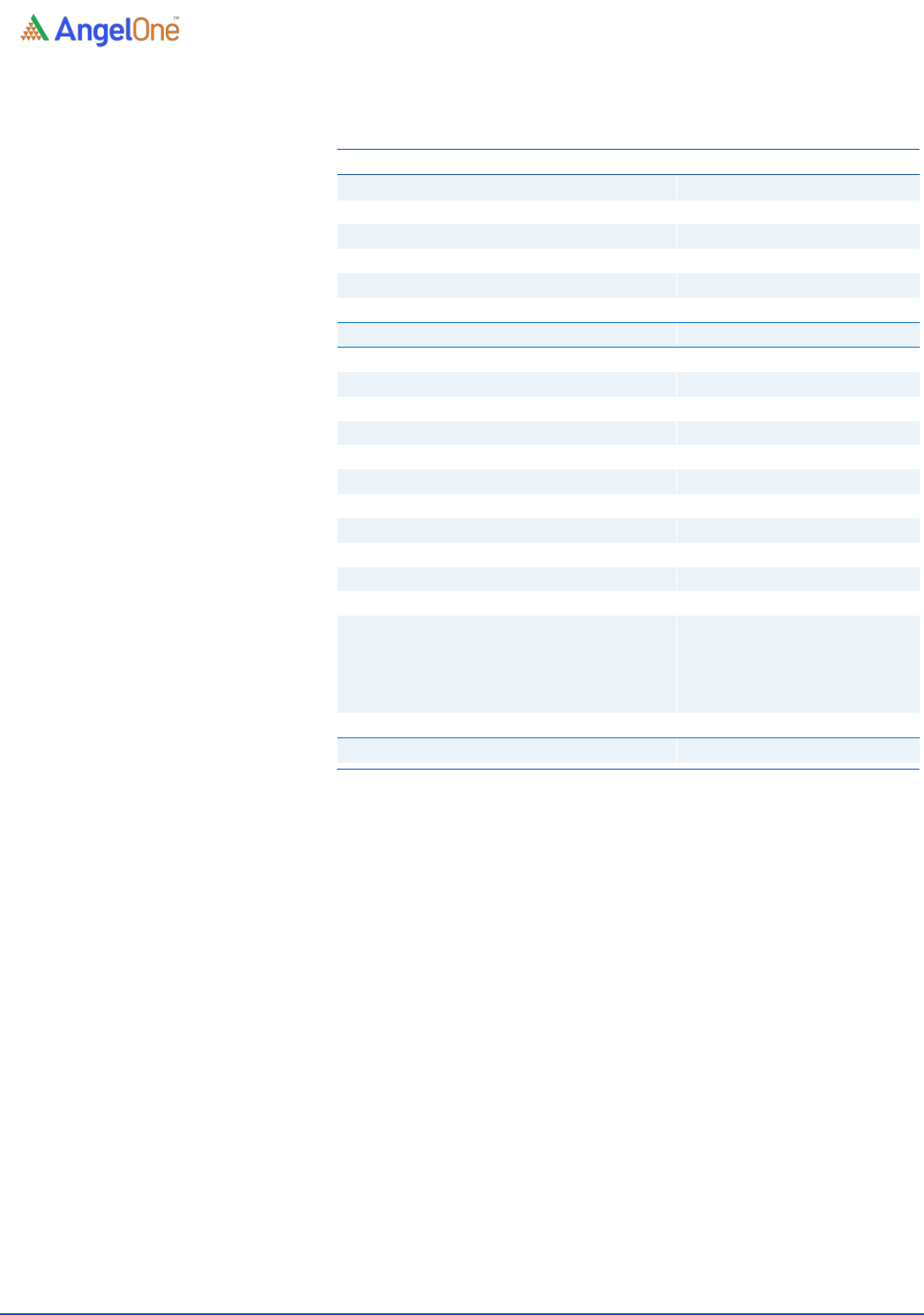

Exhibit 1: Pre and post IPO shareholding pattern

No of shares

(Pre-issue)

%

(Post-issue)

%

Promoter

5,68,43,956

79.19

4,76,45,946

61.03

Public

1,49,39,353

20.81

3,04,26,426

38.97

Total

7,17,83,309

100.00

7,80,72,372

100.00

Source: Source: RHP, Note: Calculated on upper price band

Objectives of the Offer

• Repayment or pre-payment, in full or in part, of all or certain

borrowings availed by the Company

• Funding working capital requirements

• Purchase of equipment’s and funding of other related costs for

data centers proposed to be set-up in India and overseas locations

• Funding of expenditure relating to product development

• Investment in eMudhra INC for augmenting its business

development, sales, marketing, and other related costs for future

growth

• General corporate purpose

eMudhra Limited | IPO Note

May 18, 2022

3

Consolidated Profit & Loss Statement

Y/E March (` cr)

FY2019

FY2020

FY2021

9MFY22

Total operating income

102

116

132

137

% chg

--

14.6

13.0

--

Total Expenditure

69

85

92

88

Operating expenses

32

38

32

34

Employee benefits expense

26

29

42

35

Other expenses

12

18

18

19

EBITDA

32

32

40

49

% chg

--

(0.9)

25.0

--

(% of Net Sales)

31.7

27.4

30.3

35.9

Depreciation& Amortization

9

9

9

10

EBIT

24

23

31

39

% chg

--

(1.6)

33.5

--

(% of Net Sales)

23.3

20.0

23.7

28.5

Finance costs

0

1

1

3

Other income

0

0

1

1

(% of Sales)

0.1

0.3

0.7

0.8

Recurring PBT

23

23

30

36

% chg

--

(3.3)

33.7

--

Exceptional item

2

-

-

-

Tax

4

5

6

6

Non-Controlling Interest

-

2

8

(0)

PAT (reported)

17

17

17

31

% chg

-

(4.5)

4.9

-

(% of Net Sales)

17.2

14.3

13.3

22.3

Basic & Fully Diluted EPS (Rs)

2.2

2.4

3.2

3.9

Source: Company, Angel Research

eMudhra Limited | IPO Note

May 18, 2022

4

Consolidated Balance Sheet

Y/E March (` cr)

FY2019

FY2020

FY2021

9MFY22

SOURCES OF FUNDS

Equity Share Capital

35

35

35

35

Other equity

41

57

72

105

Shareholders’ Funds

76

92

107

140

Total Loans

28

41

51

58

Other liabilities

4

6

15

5

Total Liabilities

107

139

174

204

APPLICATION OF FUNDS

Property, Plant and Equipment

15

15

66

66

Right-of-use assets

-

-

13

11

Capital work-in-progress

22

40

4

22

Intangible assets

47

47

46

51

Non-Current Investments

0

0

14

-

Other Non-Current Asset

1

2

4

8

Current Assets

35

53

45

95

Inventories

0

1

1

2

Investments

-

0

0

-

Trade receivables

21

23

15

53

Cash and Cash equivalents

2

9

8

14

Loans & Other Financial Asssets

3

3

3

3

Other current assets

8

16

19

23

Current Liability

12

20

18

50

Net Current Assets

23

34

27

45

Total Assets

107

139

174

204

Source: Company, Angel Research

eMudhra Limited | IPO Note

May 18, 2022

5

Consolidated Cash Flow Statement

Y/E March (`cr)

FY2019

FY2020

FY2021

9MFY22

Operating profit

22

23

31

37

Net changes in working capital

(10)

(4)

5

(26)

Cash generated from operations

9

8

8

11

Direct taxes paid (net of refunds)

(3)

(4)

(4)

1

Net cash flow from operating activities

17

23

41

23

Purchase of Assets

(38)

(23)

(21)

(34)

Interest received

0

0

1

0

Others

6

(6)

(27)

4

Cash Flow from Investing

(32)

(29)

(47)

(30)

Repayment (long term borrowings)

8

7

(4)

0

Repayment (short term borrowings)

3

5

(4)

14

Share issue expenses

-

-

-

-

Interest paid

-

-

(0)

(1)

Interest on Lease liabilities

-

-

15

(2)

Dividend Paid

(0)

0

(3)

3

Cash Flow from Financing

10

12

5

13

Inc./(Dec.) in Cash

(5)

7

(1)

6

Acquisition

-

-

-

-

Opening Cash balances

7

2

9

8

Closing Cash balances

2

9

8

14

Source: Company, Angel Research

eMudhra Limited | IPO Note

May 18, 2022

6

Key Ratios

Y/E March

FY2019

FY2020

FY2021

Valuation Ratio (x)

P/E (on FDEPS)

114.6

108.5

78.8

P/CEPS

77.1

74.0

58.6

P/BV

26.4

21.7

18.6

EV/Sales

19.9

17.4

15.5

EV/EBITDA

62.8

63.6

51.1

Per Share Data (Rs)

EPS (Basic)

2.2

2.4

3.2

EPS (fully diluted)

2.2

2.4

3.2

Cash EPS

3.3

3.5

4.4

Book Value

9.7

11.8

13.8

Returns (%)

ROE

23.1

18.1

16.3

ROCE

15.0

11.5

13.1

Turnover ratios (x)

Receivables (days)

77

73

41

Inventory (days)

1

6

3

Payables (days)

24

34

14

Working capital cycle (days)

54

46

30

Source: Company, Angel Research

eMudhra Limited | IPO Note

May 18, 2022

7

Research Team Tel: 022 - 40003600 E-mail: research@angelbroking.com Website: www.angelone.in

DISCLAIMER

Angel One Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager and investment advisor with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel

One Limited is a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide

registration number INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory

authority for accessing /dealing in securities Market.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of

the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to

determine the merits and risks of such an investment.

Angel or its associates or research analyst or his relative may have actual/beneficial ownership of 1% or more in the securities of

the subject company at the end of the month immediately preceding the date of publication of the research report. Neither

Angel or its associates nor Research Analysts or his relative has any material conflict of interest at the time of publication of

research report.

Angel or its associates might have received any compensation from the companies mentioned in the report during the period

preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings,

corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific

transaction in the normal course of business. Angel or its associates did not receive any compensation or other benefits from the

companies mentioned in the report or third party in connection with the research report. Neither Angel nor its research analyst

entity has been engaged in market making activity for the subject company.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions

and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a

company's fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our

website to evaluate the contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as

this document is for general guidance only. Angel One Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this

report. Angel One Limited has not independently verified all the information contained within this document. Accordingly, we

cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within

this document. While Angel One Limited endeavors to update on a reasonable basis the information discussed in this material,

there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel One Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or

in connection with the use of this information. Angel or its associates or Research Analyst or his relative might have financial

interest in the subject company. Research analyst has not served as an officer, director or employee of the subject company.